The Stellar Development Foundation, developers of the Stellar network, released a financial inclusion framework for judging the efficacy of emerging market blockchain projects. The framework was developed in cooperation with consultants PricewaterhouseCoopers International (PwC) and was explained in a white paper published on September 25.

Using this framework, the teams concluded that blockchain payments solutions significantly increased access to financial products by lowering fees to 1% or less. They also found that blockchain products have increased the speed of payments and helped users to avoid inflation.

Some blockchain developers claim their products can enhance “financial inclusion.” In other words, they say their products can provide services to unbanked people living in the developing world. Making this claim has become an effective way for some Web3 projects to gain funding. For example, the United Nations International Children’s Emergency Fund (UNICEF) has listed eight blockchain projects that it has helped fund so far based on this idea.

However, in their paper, Stellar and PwC argued that projects can fail to enhance financial inclusion if they don’t have a framework for evaluating what is needed for success. “As with any technological innovation, the need for robust governance and responsible design principles are key to successful implementation,” they said.

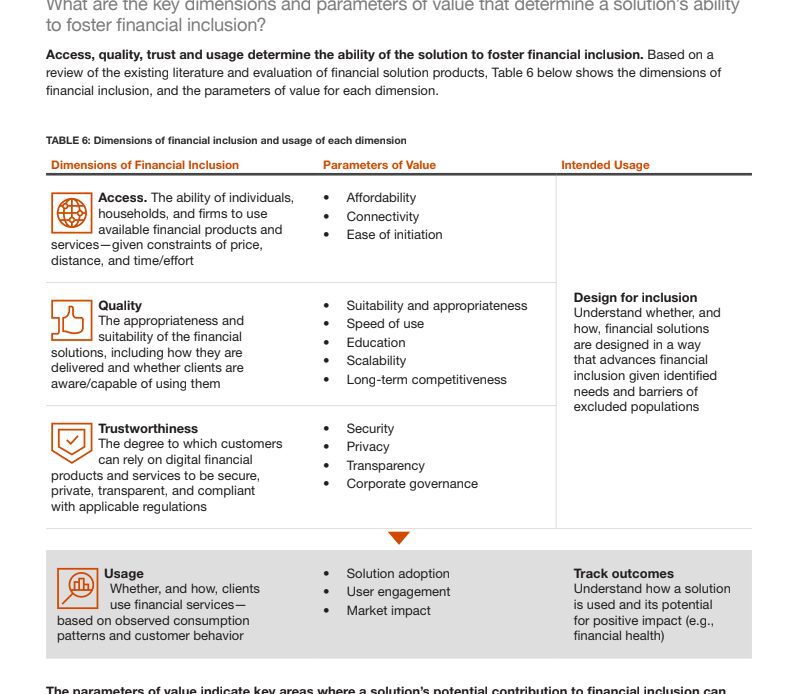

To help foster this governance, the two teams proposed a framework to judge whether a project will likely promote financial inclusion. The framework consists of four parameters: access, quality, trust and usage. Each of these parameters is broken down into further sub-parameters. For example, “access” is broken down further into affordability, connectivity, and ease of initiation.

Each explanation of a sub-parameter includes a proposed way of measuring it. For example, Stellar and PwC list “# of CICO [cash in/cash out] locations within relevant target population region” as a way of measuring the “connectivity” metric. This is intended to help ensure that projects can scientifically measure their effectiveness instead of relying on guesswork.

The teams also suggested a four-phase assessment process that projects should undergo to solve a financial inclusion problem. The project should identify a solution, target population, and relevant jurisdiction in the first phase. In phase 2, they should…

Click Here to Read the Full Original Article at Cointelegraph.com News…